Shkruar nga Pamfleti

Shkruar nga Pamfleti

The annual report of the Supreme State Audit Office is published...

Citizens' taxes continue to be "grapes and plums". The Supreme State Audit has revealed that during the past year there was 16 billion lek economic damage to the budget due to abuses in the administration. The data has been published in the annual report for 2024, a report that has already gone to the Parliament.

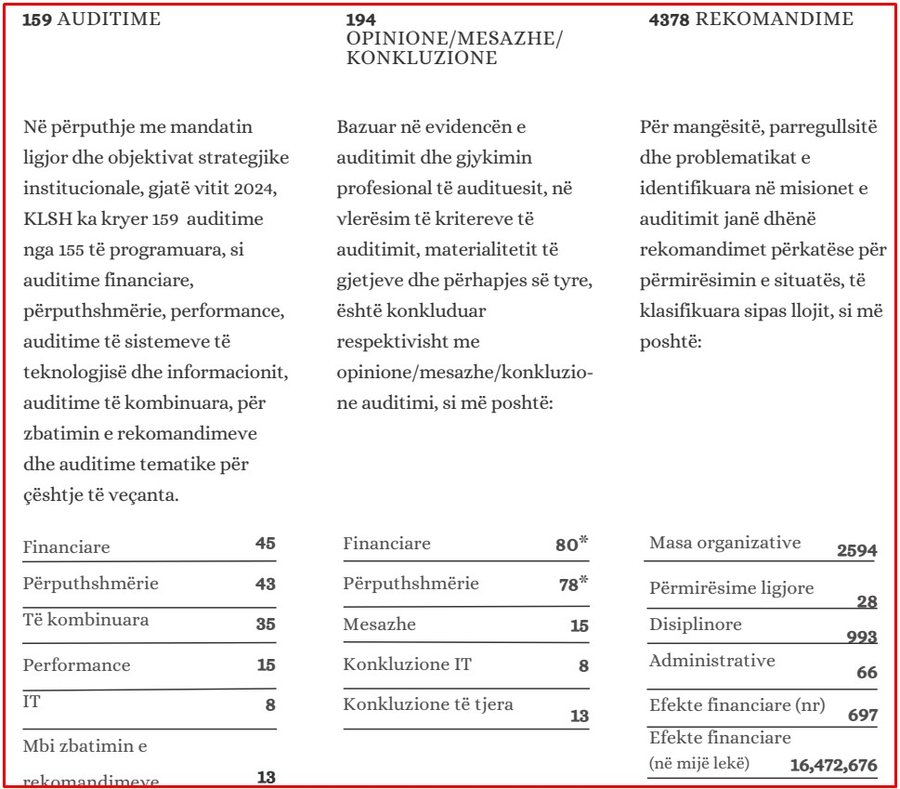

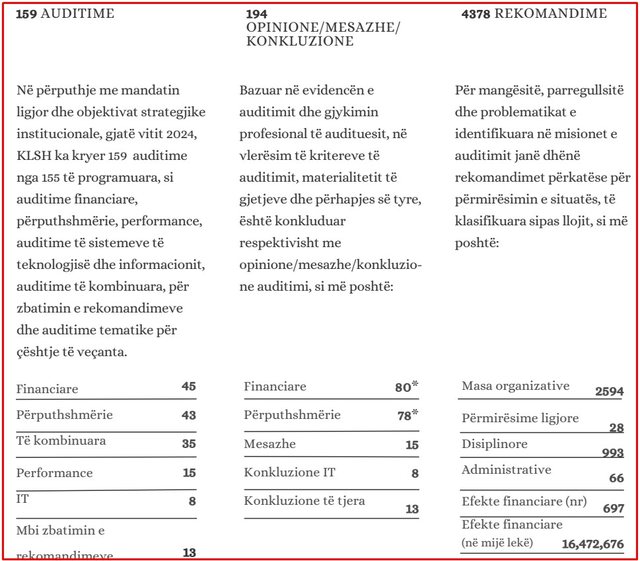

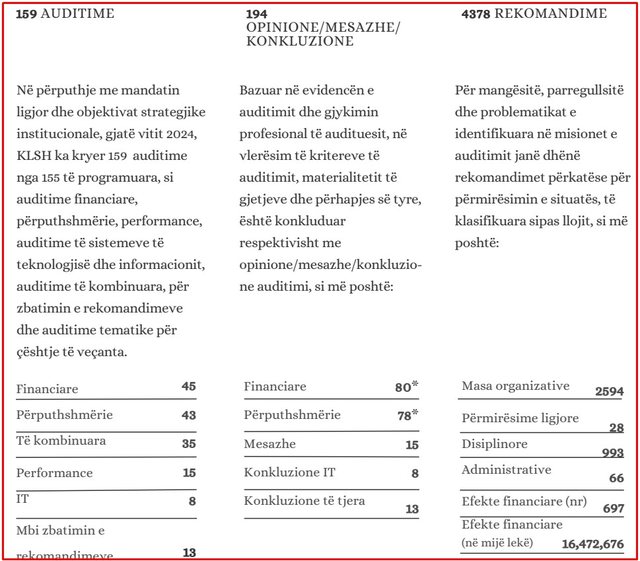

The Albanian Supreme Audit Institution (ALSA), in its capacity as the external public audit institution, has carried out a total of 159 audit missions in public institutions during 2024, which include financial audits, compliance audits, performance audits, IT system audits, combined audits, thematic audits, and verification audits for the implementation of recommendations. These audits revealed 16,472,676,000 lek of economic damage.

In financial and combined audits, a number of problems have been identified that affect the quality of financial reporting and compliance with accounting principles and standards. One of the most widespread phenomena is related to the misclassification of expenses and income, which leads to the distortion of the financial statements of institutions and undermines their credibility. Thus, cases of recording investment expenses as operating expenses, or of realized income that were not recognized in the statements at the appropriate time, have been identified, as in some central and local institutions. These problems stem from the lack of supporting documentation and the weakness of internal controls.

During 2024, the SAI conducted several compliance and combined audits, with the aim of assessing compliance with the legislation and regulatory framework in force by public institutions.

Overall, compliance audits have identified a widespread lack of compliance with the legal and regulatory framework, in procurement, fiscal reporting, contract implementation, etc. These problems are systemic and present at several levels of government.

One of the most widespread phenomena is the lack of budgetary discipline in all links of the financial cycle, including planning, approval, execution and reporting. In some cases, reallocations of funds towards projects that have not gone through the full evaluation process have been observed, accompanied by inefficient use of available funds.

Janë konstatuar mangësi në planifikimin buxhetor bazuar në vonesat dhe pasaktësitë në përgatitjen e kërkesave buxhetore nga ministritë e linjës, duke dorëzuar dokumentacion jo të plotë dhe kërkesa shtesë përtej tavaneve të miratuara, për të cilat KLSH rekomandoi forcimin e disiplinës buxhetore dhe respektimin strikt të afateve, formateve dhe argumentimit të projekteve të reja gjatë hartimit të projektbuxhetit vjetor dhe atij afatmesëm (PBA).

Shkelje të përsëritura janë konstatuar në drejtim të respektimit të afateve ligjore të regjistrimit të urdhrave të prokurimit, të kontratave dhe të likuidimit të faturave në SIFQ. Ky fenomen është përhapur në mënyrë të gjerë në njësitë e vetëqeverisjes vendore, por është i pranishëm edhe në institucionet qendrore dhe shoqëritë publike.

Në fushën e administrimit të kontratave të Partneritetit Publik Privat (PPP) dhe koncesioneve, janë konstatuar shkelje të kritereve të financimit, mangësi në monitorim dhe në vlerësimin e efekteve buxhetore afatgjata. Në disa raste është vijuar me pagesa për shërbime që nuk janë kryer, ose që janë kryer në vëllime më të ulëta se projeksioni. Fenomene të tilla janë vërejtur në kontrata të rëndësishme në fushën e shëndetësisë, ku raportimi i shpenzimeve ka tejkaluar buxhetet e miratuara dhe detyrimet janë likuiduar në kundërshtim me përmbajtjen kontraktore, përfshirë edhe TVSH-në.

Auditimet e realizuara gjatë vitit 2024, konstatuan problematika në fushën e prokurimeve, të përhapura në institucione të administratës qendrore dhe vendore, universitete, spitale dhe ndërmarrje publike. Ato lidhen kryesisht me planifikimin joefektiv të prokurimeve, kufizimin e konkurrencës, parregullsitë në hartimin dhe zbatimin e kontratave, si dhe me mungesën e kontrollit të brendshëm. Në bashkitë e audituara, planet vjetore të prokurimit shpesh nuk ishin të harmonizuara me buxhetet apo nevojat reale. Në disa raste, kriteret e kualifikimit janë vendosur në mënyrë të tillë që kufizonin garën, ndërsa në të tjera mungonte dokumentacioni mbështetës për vlerësimin dhe përzgjedhjen e operatorëve. Gjithashtu janë konstatuar procedura me vetëm një operator konkurrues, dokumente të tenderit me kritere të pajustifikuara ose të njëanshme, si dhe përcaktim i paargumentuar i fondit limit. Në disa raste, është përdorur prokurimi për shërbime që mbuloheshin nga kontrata ekzistuese, duke çuar në dublim të kostove. Ndërkohë janë konstatuar vonesa në zbatimin e kontratave, mungesë aplikimi penalitetesh, pagesa për punime të pakryera apo të realizuara në mënyrë të pa plotë. Struktura e mbikëqyrjes teknike dhe e administrimit të kontratave shpesh mungon ose nuk funksionon siç duhet.

Problems in the administration of human resources in various public institutions were also identified. One of the most repeated findings was related to unfair dismissals and the lack of supporting documentation for the relevant decisions. Cases were identified where dismissals were made in violation of the Labor Code and specific civil service laws, without a regular disciplinary process or without providing an opportunity for appeal. These practices have brought additional costs to the state budget, for the decisions of the court winners. /Pamphlet

Lini një Përgjigje