Shkruar nga Pamfleti

Shkruar nga Pamfleti

Why is the Kremlin not worried by the threat of new sanctions targeting Russian oil exports?

US President Donald Trump announced on Monday that the US could impose 100% secondary sanctions on any country that does business with Russia if a ceasefire agreement in Ukraine is not reached within 50 days.

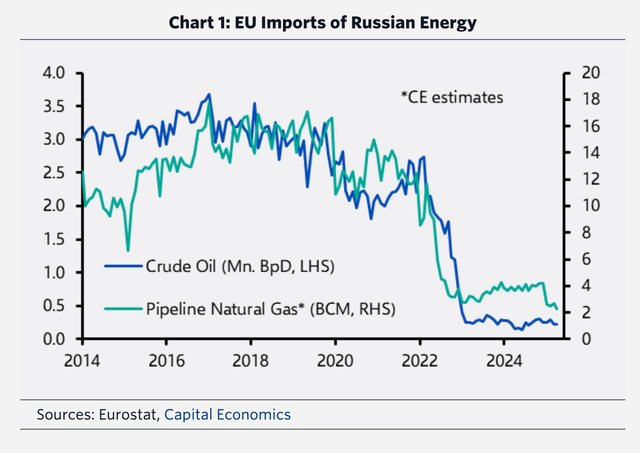

He's looking at you, China and India, which are now buying the bulk of Russia's crude oil exports after the EU imposed sanctions on exports in 2022.

Russia typically exports about 5 million barrels of oil per day (bpd), most of which goes to Asia. But what will happen to energy markets if Trump’s new tariffs effectively destroy that business? A significant drop in Russian energy flows would almost certainly lead to higher global prices, particularly for natural gas, Capital Economics wrote in a note the same day.

"The impact would probably be bigger on natural gas prices than on oil prices," said Kieran Tompkins, senior climate and commodities economist at Capital Economics. He added that this would depend on the extent to which OPEC+ intervened and covered the oil supply shortfall.

He added that such a move could cause "severe fiscal strains for Russia, but Putin's actions so far suggest that spending on the military may take priority over other expenses."

So far, the Kremlin has not been fazed by the threat of new sanctions targeting Russian oil exports. Deputy Prime Minister Alexander Novak said earlier that Russia is already accustomed to sanctions and doubts that the secondary sanctions proposed by Trump will have any impact.

The EU has also been frustrated by the ineffectiveness of oil sanctions, which have largely proved to be a wasted effort. As part of the 18th sanctions package currently being negotiated, the EU unilaterally proposed to adopt a floating oil price cap of 15% below market prices for Urals blend crude, Russia’s main export. Previously, the cap had been set at $60, but Russia has successfully evaded the sanctions thanks to its shadow fleet. Since the regime was introduced three years ago, not a single barrel of Russian oil has been sold below the $60 cap. Some Europeans called for the cap to be lowered to $45 after oil prices fell to around $60 last month, but the US vetoed the idea, fearing it would raise prices at the pump ahead of midterm elections next year.

Detajet e tarifave të reja nga Shtëpia e Bardhë mbeten të paqarta, por administrata duket se është e vendosur të vendosë tarifa 100% për importet amerikane nga Rusia dhe për importet nga çdo vend që blen energji ruse, përveç nëse arrihet së shpejti një marrëveshje për t'i dhënë fund luftës.

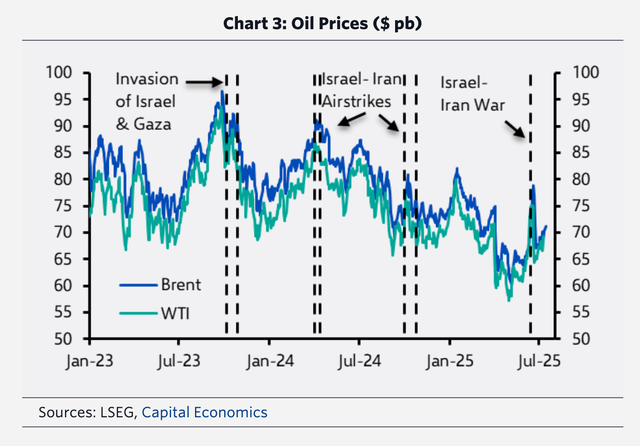

Liam Peach, Ekonomist i Lartë i Tregjeve në Zhvillim në Capital Economics, vuri në dukje se reagimi i menjëhershëm në tregun e naftës ishte i heshtur. "Çmimi i naftës bruto Brent ka rënë me pak më shumë se 1%, duke zbutur një pjesë të rritjes së të premtes", tha ai.

Kjo mund të pasqyrojë pritjet e tregut se afati 50-ditor lë hapësirë për të shmangur përçarjet dhe se tarifat e propozuara janë më të ulëta se norma 500% e përcaktuar në Aktin e Sanksionimit të Rusisë të vitit 2025 të senatorit Lindsey Graham, sipas Peach.

“Preferenca e Trump ka qenë t’i japë përparësi çmimeve të ulëta të naftës mbi nxitjen e prodhimit vendas të naftës, gjë që sugjeron se ai mund të shmangë të paktën ndërprerjet e mëdha të tregut të naftës”, shtoi Peach.

Ai gjithashtu theksoi se Akti i Sanksioneve ndaj Rusisë përfshinte përjashtime për interesat e sigurisë kombëtare, një mekanizëm që Trump mund ta përdorë për të parandaluar rritjet e ndjeshme të çmimeve.

Por nëse tarifat zbatohen plotësisht, atëherë ndikimi në tregjet e energjisë do të jetë i konsiderueshëm. Rusia eksportoi rreth 3.3 milionë fuçi naftë bruto me transport detar në ditë në vitin 2024, kryesisht në Kinë dhe Indi, dhe 1.3 milionë fuçi shtesë në ditë nëpërmjet tubacionit. Në total, eksportet ruse të naftës bruto përbënin pak më pak se 5% të konsumit global të naftës.

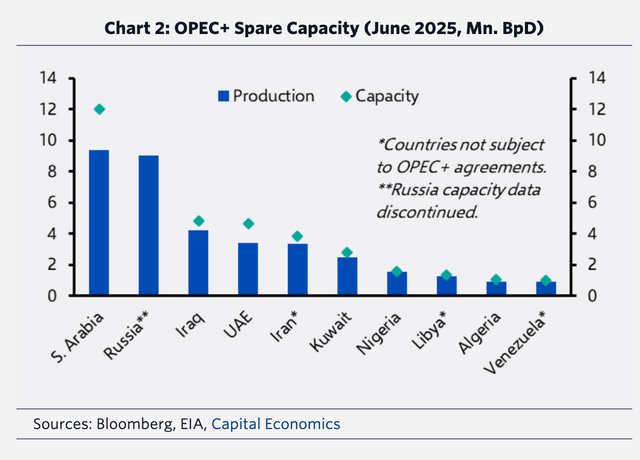

“Tregu i naftës duket se ka kapacitet të mjaftueshëm rezervë për të kompensuar pak a shumë humbjen e eksporteve ruse”, vuri në dukje Tompkins, duke treguar 5.5 milionë fuçi rezervë në ditë të mbajtur nga OPEC+ (duke përjashtuar Rusinë) që nga qershori. Megjithatë, shumica e këtij kapaciteti tashmë po tërhiqet.

"Shfrytëzimi i pjesës më të madhe të kapacitetit rezervë të botës do ta ndryshonte gjerësisht balancën e rreziqeve në mënyrë që ato të bëheshin simetrike", tha ai, duke shtuar se "heqja e atij kapaciteti rezervë do të ishte e ngjashme me ngarjen e një biçiklete pa amortizatorë, çmimet e naftës do të ndienin çdo tronditje nga çdo goditje ekzogjene."

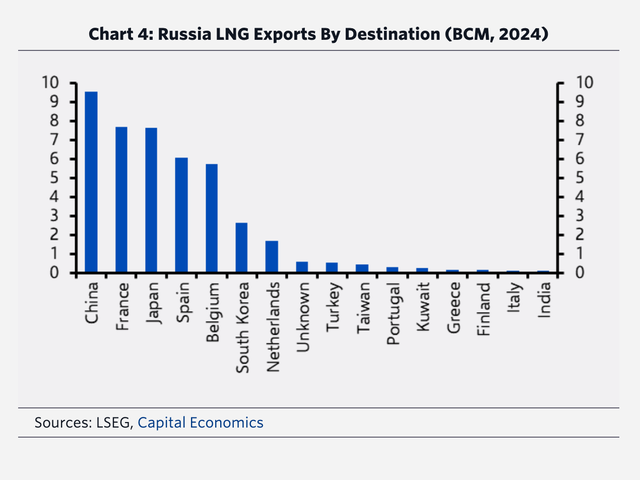

Tregu i gazit natyror mund të përballet me efekte edhe më të ashpra. Rusia përbënte 8% të eksporteve globale të LNG-së vitin e kaluar, me vëllime të konsiderueshme që shkonin në vendet brenda orbitës gjeopolitike të SHBA-së, përfshirë BE-në, e cila mbetet një nga klientët më të mëdhenj të Rusisë.

Rusia gjithashtu përbënte 20% të importeve të kombinuara të gazit të LNG-së dhe gazit të tubacioneve të Kinës, dhe ende siguronte 10% të gazit të tubacioneve të BE-së në tremujorin e parë të vitit 2025, përveç eksporteve të saj të LNG-së në Evropë.

Tompkins warned that "there is currently little or no room to absorb a further loss of Russian gas supply. While a global increase in LNG supply is expected until 2027, excluding delays in the Qatar North Field project."

But cutting off Russia’s oil revenues would inflict significant damage on Russia’s budget. While the share of oil and gas revenues in Russia’s budget has fallen from about 40% before the war to about 25%-30% now, thanks to a consumer boom fueled by military Keynesianism, with non-oil and gas revenues now generating twice as much as hydrocarbon export revenues, the reduction in oil and gas revenues would again widen the federal budget deficit from already difficult levels in June.

“A 100% tariff on exports to the US would have little impact,” Peach said, noting that trade with the US was only $3 billion in 2024. But secondary tariffs that disrupt energy exports could be much more damaging.

“We estimate that Russia exported a little over $200 billion in energy products last year,” he said, adding that “halting half of Russia’s crude oil and oil exports could reduce export revenues by about $75 billion.”

This could weigh on Russia's current account surplus, estimated at $62 billion in 2024, and lead to a weaker ruble and higher bond yields. With a third of federal revenue tied to energy taxes, a significant drop in exports could cause a nasty budget deficit.

"As a general rule, a 10% decline in energy tax revenue over a year would add 0.3–0.4% of GDP to the federal deficit," Peach said.

He added that "Russia can afford such a deficit without major financing problems, but much will depend on the scale and speed of any hit to exports."

However, according to him, "Putin's decisions so far suggest that he may continue to prioritize defense spending over other forms of spending." /Adapted from Pamphlet by Intellinews/

Lini një Përgjigje